WOODEN MARKET OVERVIEW Q1/2021 Update

We believe that in such turbulent times, it is quite difficult to keep track of latest market developments. Therefore, we keep our tradition and provide you our view on the wooden market.

1. Availability of raw material

The biggest challenge now for wooden packaging manufacturers is to ensure necessary amounts of raw material for production.

High demands for wooden packaging from different industries meet very low stock levels at sawmills. Such development forces already some packaging companies to reduce the number of production shifts and slow down production capacity.

General manager of HPE Marcus Kirchner mentioned that delivery time for some assortments is currently up to 4 months. Especially for pallet boards, plywood and some special dimensions.

In the last survey made in February 2021 by German packaging association HPE members rank the biggest challenges for the coming 6 months. Results of the survey are clear. Three main challenges now and for the coming 6 months are price trend for the raw material (71 %), availability of sawn timber (60 %) and reliable deliveries from sawmills (47 %).

* Acc. to HPE survey https://hpe.de/presse.html#!/blog/posts/4.-HPE-Corona-Blitzumfrage-Holzpackmittelindustrie-kampft-mit-stark-steigenden-Holzpreisen/114

Acc. to the survey biggest price changes were noticed within the sawn timber assortments. However big price changes had to be accepted by packaging manufacturers also for Plywood and OSB:

Availability of raw material and challenges mentioned above are applicable not only for the German market but for all European or even worldwide markets.

2. US market impact

High demands and sky climbing prices on the US market are still one of the main drivers for the current turbulences in Europe. Already in 2020 European sawmills started to increase their exports to customer in US.

According to US Department of Agriculture, Foreign Agriculture Service (FAS) 3,253 Mio m3 of soft wood sawn timber was exported from Europe to US. Which means 52% increase to 2019 and is the 3rd biggest volume after 2005 (4,482 Mio m³) and 2006 (3,682 Mio m³) ever been exported to US from Europe.

Acc. to Madison’s Lumber upwards price trend for different assortments remains the same also for the first months of 2021. Latest benchmark price for standard assortment SPF KD R/L 2×4 #2&Btr was noticed per 940US $ / 1.000 bdft fob mill. Which is around 46 US $ higher compared to 2 weeks ago or only 20US $ below all times high price from September / October 2020.

3. Steel prices

As already informed in our latest market overview, steel prices started to grow already in November 2020. And also, here price trend knows currently only one direction, and this is up:

According to the industry experts such a high price level will remain till mid / end of Q2/2021.

4. Container prices

High container prices from and to Asia complicate the situation additionally, especially for the overseas customers. Container prices are currently on a sky-high level. According to the forecast of Maersk, CCO Vincent Clerc, cool off is expected only during the first half of 2021.

5. OSB and Plywood

In our latest market overviews, we spoke mainly about challenges in sawn timber supply. While now availability of OSB and Plywood is getting worse from day to day.

Here are some facts which led to such situation:

• Huge demands from US for OSB and Plywood. In 2020 USA imported 115% more OSB from EU compared to 2019. Such trend continues also in Q1/2021;

• Several fires in production of KRONOSPAN (e.g. in Strzelce Opolskie, PL and Sanem, LU) worsen the availability of OSB additionally;

• Due to longer delivery time for OSB market participants tried to order additional volumes from alternative suppliers;

• Strong rainfalls in Brazil led to disruptions in supply with round wood in plywood production. Most producers are already fully booked till end of April and don’t provide and new offers for now.

The development mentioned above led already to some negative effect on OSB and Plywood prices. For OSB producers trying to get an increase of 35-50EUR/m3 as the next step. For plywood even higher increase is expected. It should be also noted that acc. to EUWID prices for Elliotis Pine grew from Nov. 2020 to Feb. 2021 by almost 35% already!

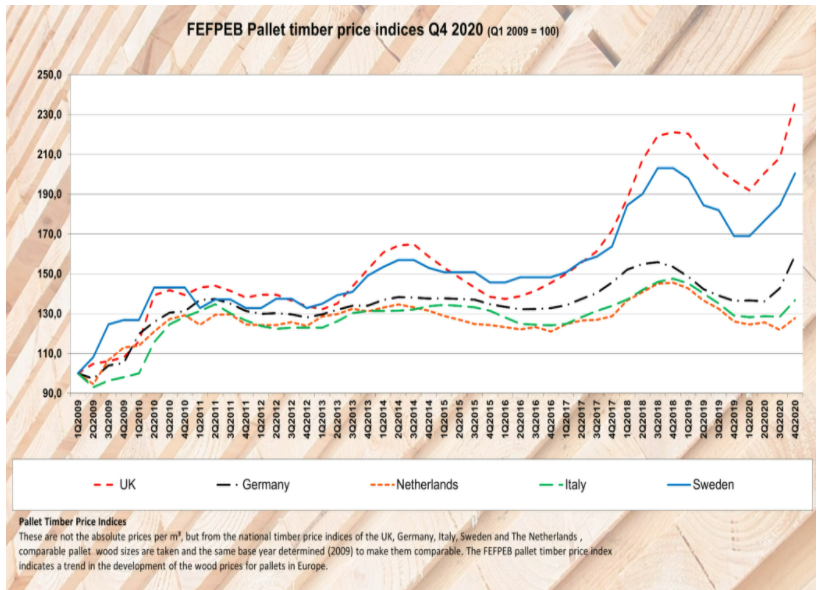

6. European Price Indices

Below you will find an overview of current available European price indices:

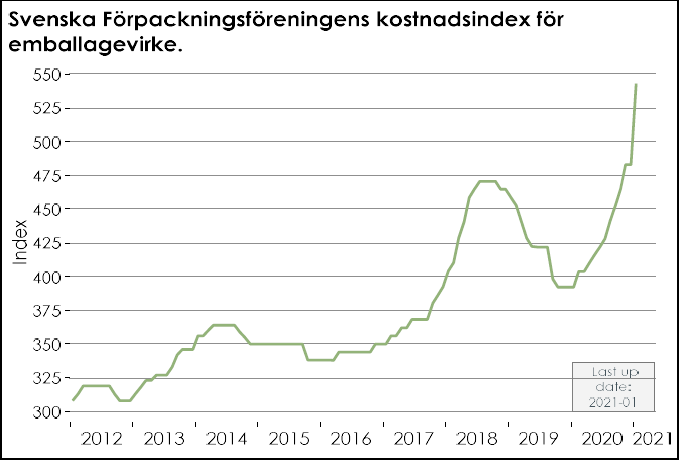

According to the Swedish wooden price index (Svenska Förpackningsföreningens kostnadsindex) raw material prices grew by 12.4 % from December 2020 till January 2021!

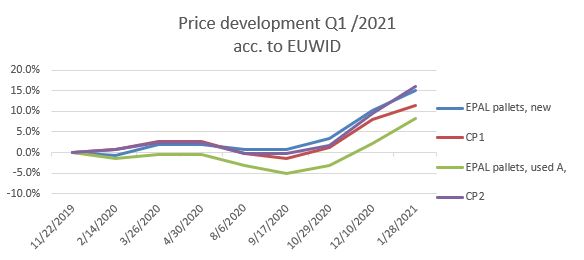

A look on the EUWID price index also shows a rapid growth for the finished goods such as EPAL and CP Pallets, started in September 2020. Prices for EPAL pallets grew by over 15% from 2020 to Feb. 2021 as shown on the chart below:

However, price indexes showing the historical price changes and give only a limited outlook on the future development of the prices. Considering huge shortage of wooden material on the market, huge demands from overseas customers and very low stock levels at sawmills we can clearly state that current price rally will remain during Q1 and most probably hold till end of Q2.

This fact must be considered for the current price negotiations with the wooden packaging end users.

7. Conclusion

Situation on the wooden market challenges us day by day. Our main goal is to secure reliable supply to our customers. Day by day our entire team working hard on this goal.

We believe that only together with you – our dear business partners, we can manage this situation and continue our great cooperation also in the coming future. Therefore, I thank you already in advance for your great cooperation and understanding of the current situation.

Sources:

https://hpe.de/presse.html#!/blog/posts/4.-HPE–Corona–Blitzumfrage–Holzpackmittelindustrie–kampft–mit–stark–steigenden–Holzpreisen/114

https://www.euwid–paper.com/markets.html

https://www.fefpeb.eu/news/press–release–pandemic–continues–to–impact–on–pallet–and–packaging–prices

https://container–news.com/msc–increases–european–outbound–rates–in–march/

https://theloadstar.com/no–happy–new–year–for–shippers–as–rates–on–major–tradelanes–stay–sky–high/

https://www.lme.com/en–GB/Metals/Ferrous/HRC–FOB–China#tabIndex=2